If you’ve ever sat down with an insurance agent in India, chances are you walked out confused. Term insurance, whole life insurance, endowment plans, ULIPs — the options feel endless. But the biggest debate, the one that actually matters for most Indian families, comes down to this: term insurance or whole life insurance?

I’ve spoken to people in their 30s who are paying ₹40,000 a year for a whole life policy thinking they’re making a smart investment. And I’ve met others who took a ₹1 crore term plan for just ₹9,000 a year and are sleeping easy at night. The difference is massive — and it’s not just about money.

Let me break this down in a way that actually makes sense, with real numbers, real examples, and honest takes. No insurance jargon, no fluff.

What Are These Two Plans, Really?

Before we compare, it helps to understand what you’re actually buying.

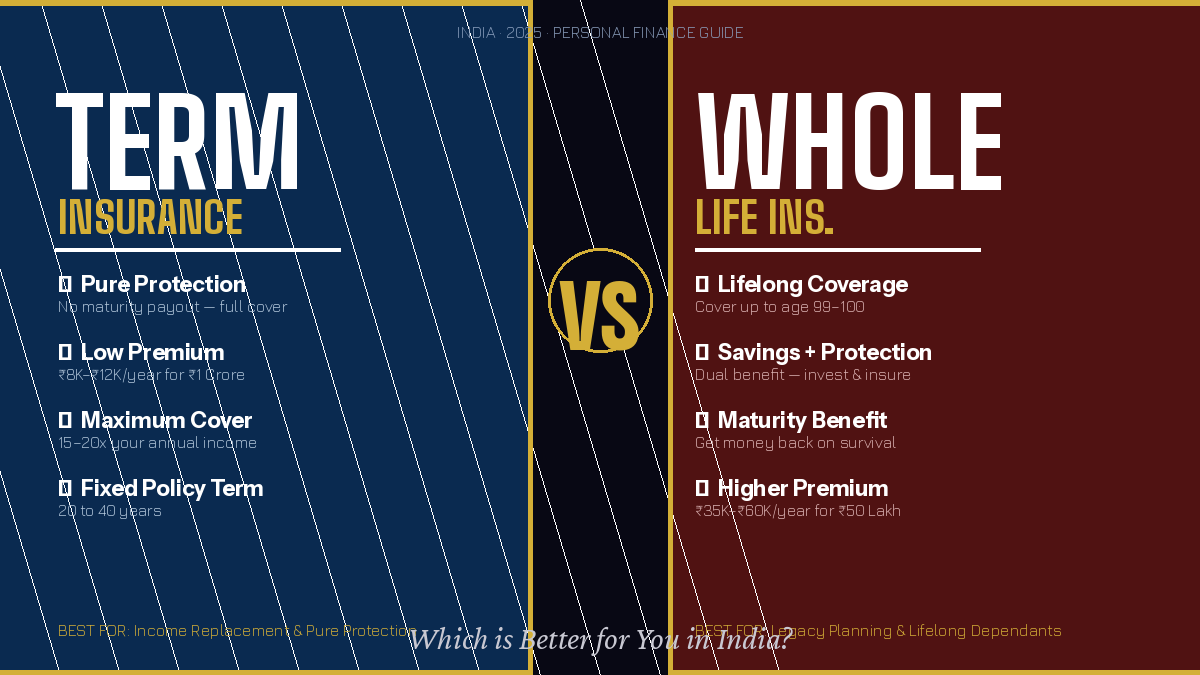

Term insurance is the simplest form of life insurance. You pay a premium every year for a fixed number of years — say 30 years. If you die during that period, your family gets the sum assured (the cover amount). If you survive, you get nothing back. That’s it. Pure protection, nothing else.

Whole life insurance, on the other hand, covers you for your entire life — usually up to age 99 or 100. You also get a maturity benefit or a savings component built in. Part of your premium goes toward life cover, and part goes into a fund that grows over time. So yes, you do get something back eventually. But as we’ll see, that “something” comes with a real catch.

The Premium Difference Is Bigger Than You Think

This is where things get interesting. Let’s take a 30-year-old non-smoker male in India as our example and compare both plans side by side:

| Feature | Term Insurance | Whole Life Insurance |

| Cover Amount | Up to ₹2 Crore+ | ₹25L–₹50L (typical) |

| Annual Premium (30yr male) | ~₹8,000–₹12,000 | ~₹35,000–₹60,000 |

| Policy Term | 20–40 years (fixed) | Whole life (up to 99) |

| Maturity Benefit | None (pure protection) | Yes, with bonus |

| Death Benefit | Full sum assured | Sum assured + bonus |

| Investment Returns | No returns | 4–6% approx |

| Tax Benefit | Sec 80C + 10(10D) | Sec 80C + 10(10D) |

A ₹1 crore term plan for a 30-year-old costs under ₹1,000 a month. A comparable whole life plan for just ₹50 lakh cover costs ₹3,000–₹5,000 a month. You’re paying four to five times more and getting half the coverage. Let that sink in.

The “You Get Nothing Back” Myth

The most common reason people avoid term insurance is the feeling that they’ll “lose” money if they survive the policy term. It sounds logical. You pay for 30 years, nothing happens, you get zero. That feels wasteful.

But this logic only works if you ignore what you could do with the money you saved.

Say you’re paying ₹50,000 a year for a whole life plan. A comparable term plan might cost ₹10,000. That’s ₹40,000 extra per year. If you invest that ₹40,000 every year in a mutual fund SIP at 12% returns over 30 years, you’d accumulate roughly ₹1.05 crore. Compare that to the maturity value of most whole life plans — which typically grow at 4–6% — and the math strongly favours the term plus investment approach.

Financial planners call this strategy “Buy Term, Invest the Rest” — and it’s one of the most well-tested personal finance principles in India. The insurance industry doesn’t advertise it because there’s less commission in it. But your wallet will thank you.

When Whole Life Insurance Actually Makes Sense

I don’t want to make whole life insurance sound completely useless. There are genuine situations where it works.

If you have a child with a disability who needs lifelong financial support, a whole life policy ensures there’s always a payout regardless of when you pass. Term insurance expires — and if you outlive it, your dependant is left without cover.

Whole life also works if you’re someone who genuinely cannot stick to investing. If you know you’ll spend every rupee of savings instead of putting it in a SIP, the forced discipline of whole life premiums can work in your favour over time.

For high-net-worth families focused on estate planning and guaranteed wealth transfer to heirs, whole life policies are sometimes used strategically — not as an investment vehicle, but as a way to ensure a guaranteed sum passes to the next generation without market risk.

What Most Indian Families Actually Need

Let’s be real about the typical Indian middle-class family. You’ve got a home loan, kids in school, ageing parents, maybe a car EMI. Your biggest financial risk is that the primary earner dies too soon, leaving everyone without income.

For this, term insurance wins — and it isn’t even close. The goal is maximum coverage at minimum cost. A ₹1–2 crore term plan at ₹10,000–₹15,000 a year does exactly that. It replaces your income, pays off the home loan, and keeps your family’s life on track.

Whole life insurance was never really designed for income replacement. It’s built for long-term legacy planning — which is a very different need.

Tax Benefits: Both Policies Are Equal Here

Both term and whole life insurance premiums qualify for deductions under Section 80C of the Income Tax Act, up to ₹1.5 lakh per year. The death benefit and maturity proceeds are also tax-free under Section 10(10D), subject to certain conditions.

One thing to watch — if your premium exceeds 10% of the sum assured (which can happen with some whole life plans), the maturity benefit may become partially taxable. Always verify this with your agent or a tax advisor before signing anything.

Best Term Insurance Plans in India (2025)

If you’ve decided term insurance is the right call, here are some of the most trusted options available right now:

- LIC Tech Term — Government-backed, widely trusted, great claim settlement record

- HDFC Life Click 2 Protect Super — Flexible options including monthly income payout for your family

- ICICI Prudential iProtect Smart — Strong claim settlement ratio, good rider options

- Max Life Smart Secure Plus — Offers return of premium variant if you want something back on survival

- Tata AIA Sampoorna Raksha Supreme — Competitive pricing with high claim settlement ratio

Always compare plans on Policybazaar or Ditto Insurance before buying. Look at the claim settlement ratio (anything above 95% is solid), solvency ratio, and what riders are available. Don’t just go for the cheapest — go for the most reliable.

The Final Verdict

If you’re a salaried professional, a business owner, or anyone with people depending on your income — go with term insurance. Get a cover of at least 15 to 20 times your annual income, ideally with a critical illness rider added on top. Then invest the premium difference in index funds or SIPs.

If you have a lifelong dependent, significant estate planning needs, or you know you’ll never invest on your own, whole life insurance has a place in your plan — but go in knowing the returns are lower than what a disciplined mutual fund investor would get.

The truth is this: insurance is for protection. The moment you start expecting it to grow your wealth, you’re usually paying extra for something a better investment could do more efficiently. Keep your protection and your investments separate — and you’ll be in a much stronger financial position over time.

Pro Tip: Before you buy any insurance policy, consult with a SEBI-registered fee-only financial advisor or use the Ditto Insurance advisory service. They don’t earn commission on sales, which means their advice is genuinely in your interest — not the insurer’s.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Please consult a certified financial planner or insurance advisor before making any decisions.